Begin with a month that you promise not to judge. Capture spending without attempting to reform it. The point is baseline truth, not immediate virtue. Many people discover that their “mystery” hundred dollars is a collection of small conveniences—parking, delivery, minor subscriptions—that felt insignificant individually. Aggregation is a spotlight; it is not an accusation.

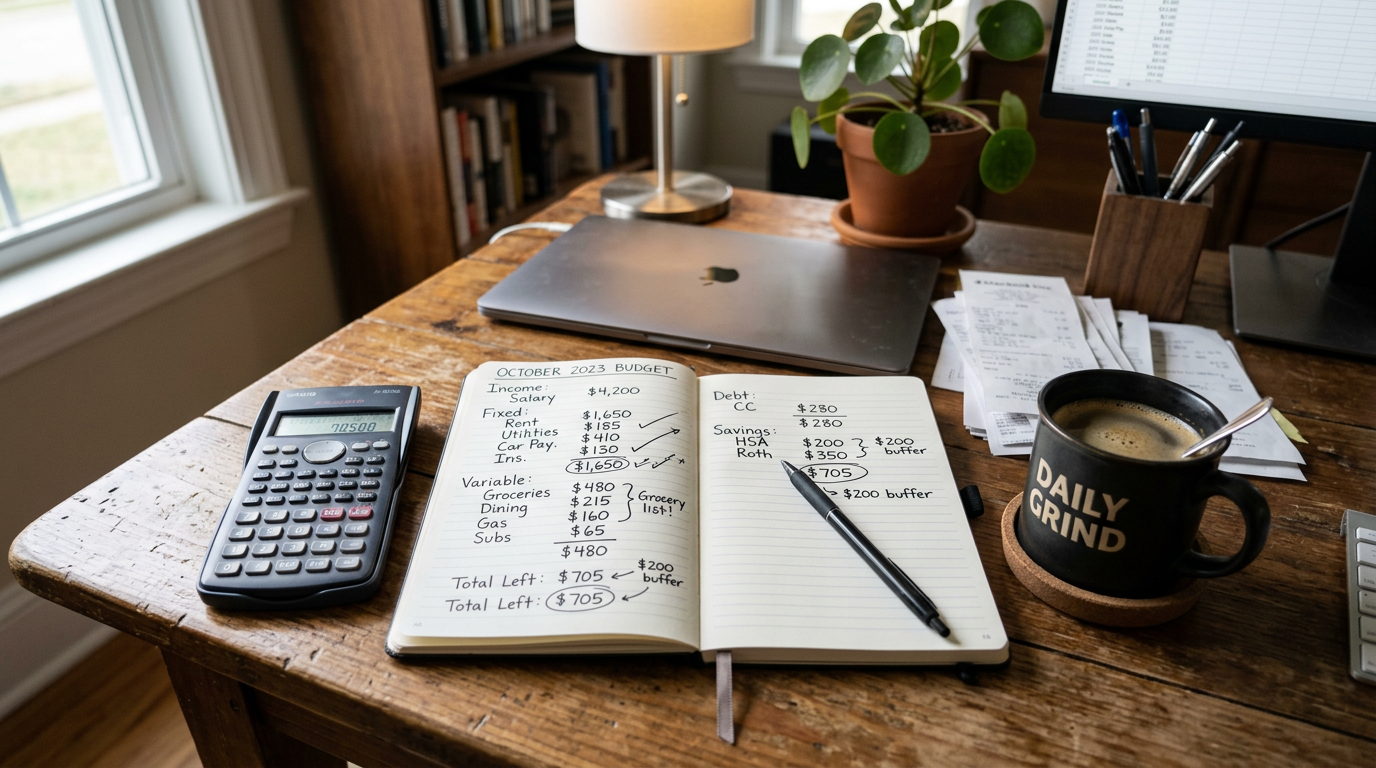

Separate fixed obligations from flexible ones, but add a third bucket: lumpy expenses. Insurance premiums, annual memberships, holiday travel, and school fees do not belong smoothed into a generic monthly average unless you also fund a sinking fund that makes the lumps survivable. A sinking fund is simply labeled cash waiting for a known future bill. It turns spikes into flat terrain.

Envelope thinking still works, even without paper envelopes. Digital pots with names reduce leakage because names carry meaning. “Dining out” and “groceries” are different emotional contracts; merging them blurs feedback. Some households thrive with a strict weekly cash amount for discretionary spending; others prefer a monthly ceiling with mid-month check-ins. The correct version is the one you can explain to a partner without a fight.

Review weekly if you are repairing habits; monthly if you are maintaining them. Weekly reviews catch drift early; monthly reviews suit stable seasons. Either way, pair numbers with a single qualitative question: did spending align with what we said mattered? Values drift too—children age, careers pivot, cities get expensive. A budget that never updates its categories ossifies into resentment.

Debt payments deserve explicit lines, not hiding inside minimums. Seeing principal versus interest clarifies the true cost of carrying balances. If you are paying down debt while investing, be explicit about why—sometimes employer matches or tax advantages justify split priorities; sometimes emotional peace argues for acceleration. The worst state is accidental: each dollar unsure of its job.

Finally, celebrate maintenance. Keeping a budget alive for a year is harder than starting one. Mark small milestones—first quarter without overdraft surprises, first holiday funded in advance—and treat them as competence signals, not moral grades. Money is a tool; shame is a blunt one.

This material is informational. It does not know your income volatility, family obligations, or regional costs. Use it to experiment gently, not to benchmark yourself against an imaginary optimal household.